US P2P market: Land of opportunity

The US dominates the global alternative lending market, but where are all the peer-to-peer lending platforms? By Kathryn Gaw

Alternative lending is flourishing in the US. According to a recent report from Allied Market Research, the global alternative finance industry generated $173.9bn (£134.42bn) in 2022, with North America accounting for almost two fifths of this.

The report predicted that by 2032, the alternatives market will generate $920.9bn, and North America will continue to dominate the sector.

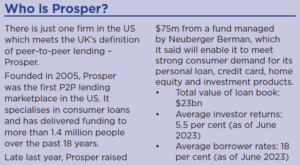

Yet peer-to-peer lending represents a small fragment of this enormous market. In fact, if we take the UK definition of P2P lending – loans funded by retail investors made on a regulated platform – there is just one lender in the US P2P market.

With a loan book value of more than $23bn, Prosper’s business is worth more than the entire UK P2P lending market combined. Like most US-based fintechs, it is headquartered in San Francisco. It offers both consumer and business loans, and is funded by a mix of both retail and institutional investors.

Given the demand for alternative finance in the US, and the success of Prosper’s business model, it is surprising that there is not more competition in the US P2P market. There are a few reasons behind this.

The first is regulation. The US P2P sector is regulated at both a federal and a state level. At the federal level, the Securities and Exchange Commission (SEC) oversees investor protections, while the Consumer Protection Financial Bureau with the Federal State Trade Commission has oversight over the borrower side.

Platforms are subject to further regulation under the laws of the state in which they are headquartered.

This creates a complicated administrative burden which can only be managed by a sizable team of highly-trained staff. Naturally, this makes it harder for smaller players to enter the market, unless they have hefty funding behind them and a wealth of regulatory and legal expertise.

In 2008, the SEC passed a law requiring all P2P platforms to list their offerings as securities, rather than loans. This was the first time that the sector came under regulatory scrutiny, and it led to a slowdown in the growth of the sector. At that stage, a handful of P2P startups had sprung up, mainly around Silicon Valley. Largely specialising in offering consumer loans to people with poor credit, these platforms were beset with high default rates from the start.

Read more: Prosper raises $75m in growth capital

More damningly, in 2021 the SEC introduced a new rule which means that American P2P lending platforms are not permitted to issue loans directly with money provided by lenders. Unsurprisingly, this led many P2P platforms to exit the retail market and pivot towards institutionally-funded lending instead.

LendingClub was a prime example of this. It left the retail market in 2020 ahead of the new SEC rule. At its peak, LendingClub was the world’s largest P2P lending platform, offering both consumer and motor loans. In 2014, it raised $1bn to launch the largest technology initial public offering of the year in the US. However, a series of scandals involving former chief executive Renaud Laplanche saw the company’s share price plunge.

In February 2020 LendingClub announced that it had agreed to buy Radius Bank for $185m, which allowed the platform to rebrand itself as an online bank, marking the official end of its P2P journey.

Read more: LendingTree adds Funding Circle US to its network

Over the years, several other P2P platforms have gone a similar route. Sofi, Kiva and Lending Point have all stopped accepting retail money and shifted towards a balance sheet lending model instead. Peerform has stopped accepting retail money altogether. LendingTree has moved into the credit card space. StreetShares was acquired by software company Meridian Link, and Credit Karma was acquired by financial software firm Intuit.

Upstart has been able to bypass the SEC rules somewhat by inviting lenders to invest indirectly in its consumer loans via its referral business. Meanwhile Prosper has used state rules to its advantage, by accepting only those investors who are registered in a P2P-friendly state. Prosper is headquartered in San Francisco, California, and maintains an office in Plano, Texas, where investor regulations are more favourable for fintech lenders.

Read more: Prosper commits to retail P2P amid LendingClub exit

Funding Circle made a splashy entrance into the US market in 2013, and went on to originate more than $4bn of small business loans in the country. However, it has since become an institutional-only platform, with no access for retail investors.

Another reason why the US P2P market seems to have stalled has to do with borrower culture. Consumer borrowers overwhelmingly choose credit cards and bank loans to meet their lending needs. According to Experian, the average American has 3.84 credit cards, making consumer loans less relevant to the wider market.

Business borrowers are also well served by the mainstream lending market, alongside alternative lenders such as Funding Circle. The bridging market is extensive, offering quick financing to both businesses and property developers.

While the alternative lending market is booming in the US, there are still limited opportunities for retail investors. At present, US investors have only one clear option if they want to invest in P2P loans – Prosper. While it is also possible to invest in P2P loans indirectly (for example, via Upstart), the barriers to entry remain high and awareness remains low.

Regulation and a culture of credit cards and mainstream lending has slowed the progress of P2P lending in the US in comparison with the UK. While the sector got off to a strong start in 2005, almost 20 years later the market has shrunk beyond recognition. Even the term ‘P2P’ is losing its meaning, as American investors use the acronym interchangeably to describe everything from equity crowdfunding to crypto trading.

However, the US market is immense and there are still gaps where traditional and alternative financing cannot reach. Credit card debt is expensive and bridging loans are only intended to be used to cover short term cashflow issues. Access to affordable lending is particularly important during an economic downturn, and while the US economy is performing better than the UK’s, interest rates and inflation are still relatively high.

If they can navigate the complexities of US P2P regulations and reach their target investor base, the next generation of US P2P lenders could take a considerable market share of the $920.9bn alternatives sector.