S&P: Rising defaults will test asset quality of private credit funds

Rising default rates will test the asset quality of private credit funds, according to S&P Global Ratings, which warned of “pockets of vulnerability” in the sector.

In a new report, the ratings agency said that private credit’s performance has been solid over the past years, but it expects default rates to rise among global corporates due to high interest rates and dislocated markets.

Read more: Moody’s downgrades three direct lending funds

“Such an increase in default rates will test the asset quality and ratings resilience of private credit funds,” S&P Global Ratings credit analyst William Edwards said.

The average rated fund could withstand a 52 per cent drawdown in asset valuations at current rating levels, according to the report, although this number may be as low as four per cent, which it said indicates that pockets of vulnerability exist among rated funds.

“While most rated funds look set to weather this period, for those with elevated leverage and tight liquidity, this test could harm their ratings,” Edwards added.

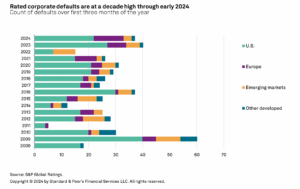

S&P said that the rising rates environment is already testing global credit quality. It cited its own data which showed that defaults in the first two months of 2024 were at their highest level since 2009.

Looking at Europe specifically, defaults more than doubled in the first two months of 2024 compared to the same period in 2023 as vulnerable borrowers struggled with expensive debt.

“Conditions are similarly strained among our global population of middle-market credit estimates,” S&P added.

Read more: Competition intensifies between private credit and syndicated loans

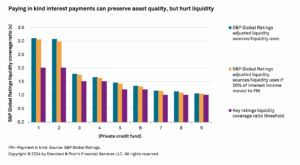

The increasingly popular payment-in-kind (PIK) structures can preserve asset quality but hurt liquidity, the report said.

These types of loans allow the borrower to make interest payments in forms other than cash, and not have to repay the interest until the loan term is ended.

Read more: Private credit to “thrive” as dry powder reaches $292bn

“These measures can preserve portfolio credit quality and give debtors breathing room,” the report said.

“That said, they can also undermine the major strength of our private credit fund ratings: their stable and predictable interest income. For the most levered funds we rate, if 20 per cent of their portfolio moved to PIK from cash payment of interest, they would likely see our view of their liquidity move very close to levels commensurate with a lower rating level.”